With the recent surge in consumer prices and emergency pandemic aid winding down, housing affordability challenges are on the rise, particularly for low-income households and households of color, according to The State of Nation’s Housing 2022 report recently published by Harvard University’s Joint Center for Housing Studies (JCHS). While the report’s focuses mostly on nationwide market trends for homeowners and renters, demographic changes and trends in housing affordability and sustainability, its look at North Carolina reveals sections of the state outpaced the nation with both home price increases and investor buyouts of single family homes.

The Increasing Cost of Homeownership

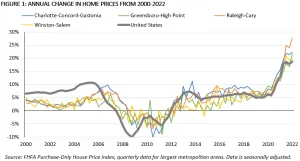

The Federal Housing Finance Agency (FHFA) House Price Index shows home prices surged 19% nationally from 2021–Q1 to 2022–Q1. Annual home price growth in all four of the largest metropolitan areas in North Carolina exceeded this national trend (see Figure 1 below). The Raleigh-Cary metropolitan area saw the largest annual home price growth from 2021–Q1 to 2022–Q1 (28%)—more than two times faster than the 14% increase a year earlier and nearly five times faster than the 6% increase two years earlier.

Investors are buying up a record share of single-family homes across the United States—especially in the South and West—leaving even fewer homes available for sale and helping drive up home prices. Nationwide, the percentage of homes sold to investors rose to 25% in the last quarter of 2021, up from the 16% averaged in 2017–2019. Once again, several of the largest metropolitan areas in North Carolina outstrip national trends: in the fourth quarter of 2021, Charlotte saw 33% of single-family home sales sold to investors (seventh in the nation among the 100 largest markets), Raleigh and Durham-Chapel Hill both saw 30%, and Greensboro-High Point and Winston-Salem both saw 27%.

Hurdles for First-Time Buyers

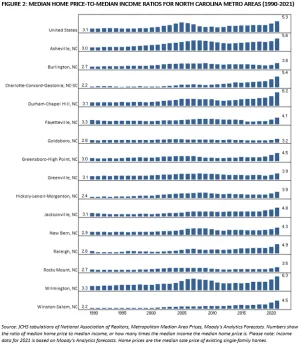

This historic home price growth helps explain why the median home price-to-income ratio across much of North Carolina has reached record highs in 2021. Data on mortgage affordability from Moody’s Analytics shows that for the 15 largest metropolitan areas in North Carolina the median sales price for existing homes in 2021 was between 3.2 and 6.3 times the median household income—well above the ratios in 2020 and a notable increase from the previous peaks in the mid-2000s. Median home price-to-median income ratios were the highest in Wilmington (6.3), Durham-Chapel Hill (6.2) and Asheville (5.6) in 2021.

On top historic home price growth, interest rate hikes in early 2022 have further eroded the affordability of home ownership across much of the United States, especially for first-time buyers. JCHS estimates that the impact on monthly mortgage payments of the average 2.0 percentage point interest rate increase between December 2021 and April 2022 is equivalent to a 27% increase in home prices. At these prices, the typical down payment (assuming 7% of sales price) that a first-time buyer would need for a median-priced home in the US is $27,400, which would rule out 92% of renters, whose median savings are just $1,500 and who are disproportionately lower-income households and households of color.

The North Carolina Housing Finance Agency offers an array of financing options designed to help address these very challenges. The Agency offers mortgage products, down payment assistance, mortgage credit certificates and community home ownership programs to help create more affordable home ownership opportunities for North Carolinians. To learn more, visit the home buyers section of www.HousingBuildsNC.com.

Read the full report at State of the Nation’s Housing 2022.